INVESTMENT PROPERTY MARKET COMMENTARY Q1-2 2021.

Vickery Holman are delighted to release the 2021 Q1 Investment Property Market update from Clare Cochrane. Against the backdrop of Brexit and long-standing uncertainty over a trade deal it is unsurprising that the Pandemic put the markets into a quandary, it is however surprising at how quickly activity has returned since Quarter 4 2020. The vaccine has offered hope towards normality and with the dust settling from the UK’s EU departure confidence is returning.

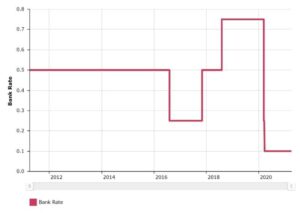

More optimistic forecasts by the Bank of England, lower unemployment projections, and historically low interest rates of 0.1% will aide confidence. Inflation is currently at 0.4%, against a target of 2%.

Source; Bank of England interest rates

Supply and Demand

Investors adopted a ‘wait and see’ philosophy during the early part of the pandemic which combined with an inability and unwillingness to travel resulted in a severe lack of stock. Transactional levels have therefore predictably been suppressed.

Demand remains significant from those looking for returns on their capital. Local Authorities, Regional Prop Co’s and Sipp investors have remained inquisitive.

Some larger investors have sold portfolios in readiness to capitalise on new opportunities from any market fall out. As however, we haven’t seen an increase in ‘fire’ sales which is largely due to low interest rates, liquidity, and government intervention bolstering the market.

Limited transactional evidence makes it hard to gain a full insight into how values have been affected but wider discrepancies in the performance of sub sectors and locations across the region are apparent.

Yields are quoted with a note of caution, with significant uncertainty in the market and large variations across the region advice should be sought on property specific opportunities. Please contact VH.

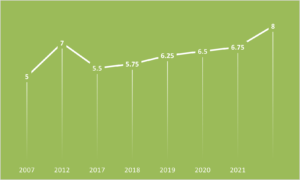

Industrial

The industrial sector remains the most resilient across the region. A surge in demand from logistics/online operators and the consequential rental increases due to low supply has increased investor appetite.

Deals done indicate a slight improvement of prime yields in some locations and no change in others. Prime opportunities therefore attracting yields of between 5.5-6%. Bristol however remains a different kettle of fish and attracts a significant premium.

Some signs of pricing and lot size affecting saleability have been evident with a couple of multi-let estates in the £1.5-£2 Million bracket remaining available for longer. Whether they are overpriced or just in a tricky lot size remains to be seen.

A question mark also remains over how sustainable the higher rents being achieved on second-hand stock are and whether the market is starting to look overheated.

Source; VH internal records. Excludes Bristol.

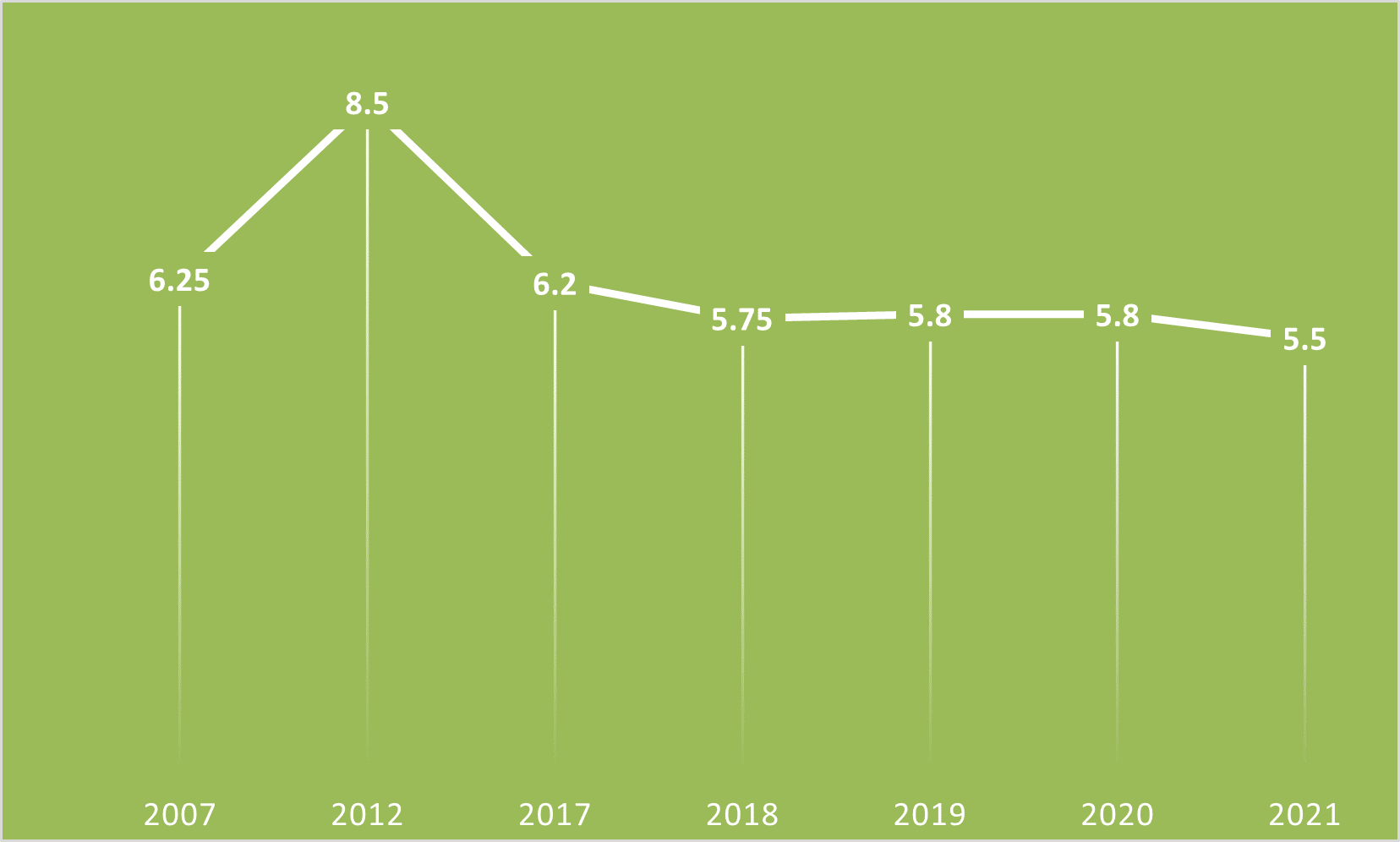

Retail

The retail sector has grappled with significant changes for several years. Covid has accelerated the trend towards online shopping adding another blow so a re-alignment of rents and values is inevitable.

Transactions have been limited, yields have softened and there is a wider discrepancy across the region than before, prime now 6.75% to 8% but rising rapidly to double figures for some assets.

There have been pockets of activity in affluent coastal locations where strong occupational demand and a rise in staycations has instilled confidence. Several- mixed-use properties recently sold for under 7%.

Retail will likely remain the most volatile sector and we anticipate values to fall disproportionately more on prime than secondary and tertiary due to greater adjustments in rent and use. Opportunities due to the re-purposing of stock to urban logistics, alternative uses and residential will however materialise and be of interest to a new type of investor.

Source; VH internal records.

Offices

Activity within the office sector has been muted, prime yields depending on where in the region typically vary from 6% plus, softening to a greater degree in locations such as Plymouth where occupational demand is poor than in the likes of Exeter. Bristol remains an exception where the market remains disproportionately strong and there were some big investment sales achieving lower yields.

As it has become clearer that companies will reoccupy renewed interest is likely in this sector and lease movement from occupiers ‘right sizing’ for their new working norm will create opportunities. Higher quality buildings, will remain favoured as ESG (environmental, social and governance) and healthy building credentials feature higher on investors decision making criteria.

Source; VH internal records. Excludes Bristol.

For further information please contact Vickery Holman, Clare Cochrane; [email protected], 01392 20 30 10, 07921 058089.

For more information on investment opportunities, please click here.